Thesis

Employer-sponsored health insurance has long been a key component of employee benefits, but increasing costs and complicated administrative demands are prompting businesses of all sizes to consider more flexible options. From 2010 to 2022, average premiums increased by almost 60% across various coverage types, outpacing inflation. In 2024, the average annual premiums reached $9K for single coverage and $25.5K for family coverage, marking yearly increases of 6% and 7%, respectively. Small firms, those with fewer than 50 employees, bore a heavier burden, with average premiums for single coverage reaching $9.1K per employee, surpassing the $8.9K average at large companies. For these employers, the financial pressure is compounding: between 2018 and 2023, health insurance premiums grew faster than any other operating expense, pushing the median insurance burden from 3.3% to 4% of total operating expenses.

Offering competitive benefits is increasingly difficult for companies with limited resources, and the administrative complexity of managing group plans only adds to the strain. As a result, many employers opt out entirely, either never offering coverage or eventually dropping it. In 2023, only 49.2% of private sector small firms offered health insurance, compared to 97.6% of large firms. Furthermore, every 10% increase in health insurance costs raises the likelihood of small firms discontinuing coverage by 1.3% to 2.6%, depending on the industry. This widening gap not only leaves millions of workers without employer-sponsored coverage but also puts small businesses at a structural disadvantage in attracting and retaining talent.

One solution to this problem, rooted in 2020 legislation, is the Individual Coverage Health Reimbursement Arrangement (ICHRA). It enables firms to reimburse employees tax-free for individual health insurance premiums and medical expenses, instead of providing a traditional group health plan. Workers would willingly forgo 10% to 40% of the health insurance funds their employers pay in exchange for control over choosing their own plan. ICHRA enables this consumer choice by shifting plan selection from HR to individuals, allowing employees to pick coverage that better fits their needs, providers, and locations. Early data shows participants select higher-quality, better-suited plans and value the ability to match coverage with their preferred doctors and networks.

Looking at employers, healthcare costs reached $14.8K per employee in 2024, rising 8% to 9% annually for two decades. ICHRA addresses rising costs by shifting from a defined benefit to a defined contribution model. It allows employers to set fixed, pre-tax stipends and gain predictable budgets, while employees can supplement their coverage. Thus, small businesses can offer coverage more effectively; 80% of small firms offering ICHRA are offering health insurance for the first time as of 2025. At the same time, 72% of small-business leaders said they were not familiar with ICHRAs, which is a potential strong demand tailwind.

Thatch allows businesses of all sizes to offer their employees a personalized healthcare and benefits experience. Established by a founding team with a strong healthcare and fintech background, Thatch is an ICHRA administrator with a payment architecture to support money flow across all healthcare benefits stakeholders. Thatch offers a platform where employees can select personalized healthcare plans (medical, dental, and vision) within a defined budget and use the Thatch marketplace and debit card for any remaining healthcare expenses. Beyond this consumer-facing experience, Thatch’s strategic focus is on exposing its infrastructure via APIs, enabling third-party administrators, brokers, carriers, payroll vendors, and other partners to embed ICHRA solutions into employer workflows seamlessly.

Founding Story

Chris Ellis (CEO) and Adam Stevenson (President) founded Thatch in October 2021. Both founders experienced the loss of a parent to cancer during their formative years, witnessing firsthand the complexities and challenges of navigating healthcare payments during an already difficult period.

Ellis worked in healthcare before founding Thatch, beginning his career as a cancer researcher at MIT before transitioning to commercial roles. He established the US sales division at clinical software startup Sophia Genetics and later contributed to product development at Agilent, a prominent biotech firm.

Stevenson’s experience blends fintech and healthcare. He spent four years at Humana while launching several successful bootstrapped ventures on the side. Stevenson then joined Stripe, where he spent seven years building and leading multiple customer engineering teams.

The two founders met in the summer of 2021 and started exploring various opportunities in healthcare. They identified a consistent theme: While clinical care delivery had seen significant advances, the fundamental challenge of healthcare payment remained a persistent source of friction for both enterprises, which struggle with administration and rising costs, and their employees, who faced more limited options as a result. This insight, alongside a crucial change in legislation, became the foundation for Thatch's mission to transform the healthcare benefits experience.

As of April 2026, Thatch has close to 200 employees. Ellis and Stevenson have assembled an experienced early team, attracting many individuals from Stripe, as well as folks from Ramp*, Rippling, Robinhood, Shopify, Google, and other top companies. In April 2025, Thatch hired former United Healthcare CEO Gary Daniels as Chief Growth Officer.

Product

At its core, Thatch is a fintech platform that helps businesses provide their teams with flexible health benefits. The Thatch platform is built around ICHRA (Individual Coverage Health Reimbursement Arrangements), a 2020 regulatory change allowing employers to reimburse employees for individual insurance premiums as an alternative to group health insurance.

Employees can use this money to select their own health plans from the individual marketplace rather than employers forcing specific plans on them, and any money left over is saved in the employee account and can be allocated to prescriptions, therapy, or any other qualified medical expenses using the Thatch debit card. In Ellis’s view:

“Patients should be empowered to make choices across the healthcare ecosystem, whether that’s the hospital they visit, the insurance they choose, or the digital health products they use. We want to give patients the flexibility to vote with the healthcare dollars they get from their employer so insurance carriers start to care about building loyalty based on the experience they provide.”

Employer Platform

Thatch’s core product is a Third-Party Administrator (TPA) platform that enables businesses to provide flexible healthcare benefits to their employees. Thatch handles the entire process, including onboarding, plan selection, payroll, reimbursements, and compliance.

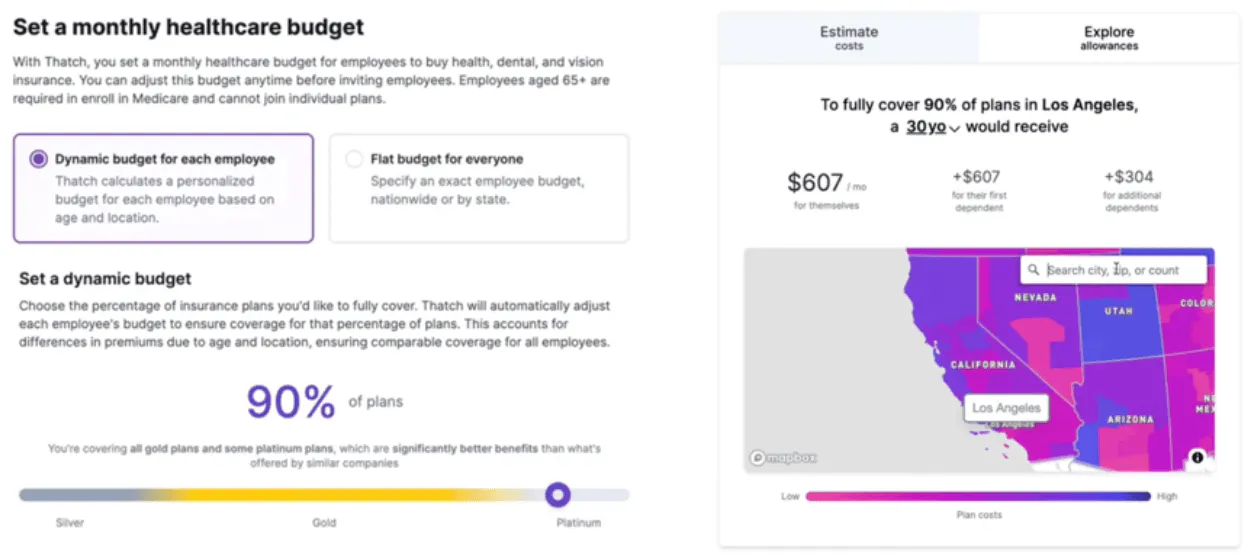

Instead of contracting an insurance broker or polling employees, businesses can input basic information about their company and set a healthcare budget. Thatch then channels this budget directly to employees, who can use the platform to personalize their healthcare experience.

When onboarding, a company selects a budget for each employee by either deciding on a flat rate or benchmarking its budget against Thatch’s data across companies, states, and employee demographics. ICHRAs can be more cost-effective for businesses, especially SMBs, because of their defined-contribution nature, which makes healthcare benefits more predictable for employers.

Source: Thatch

Employee Platform

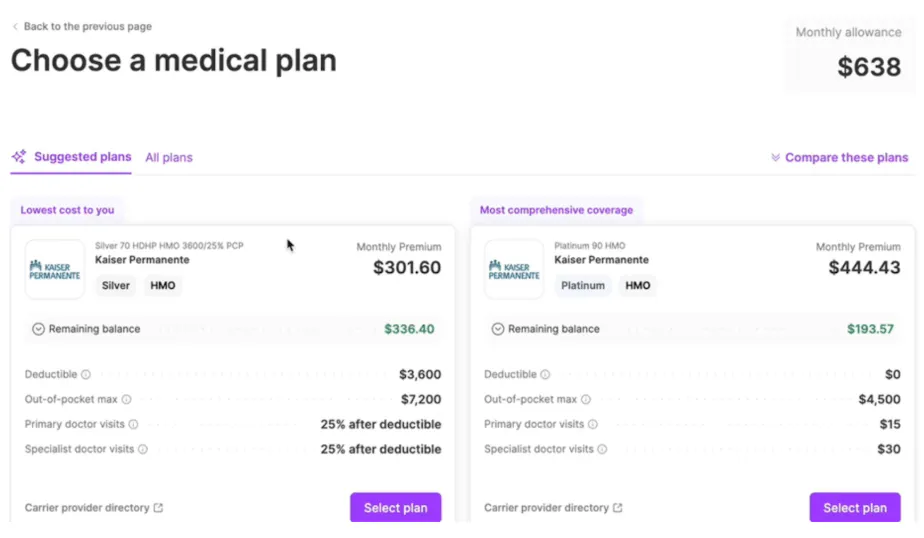

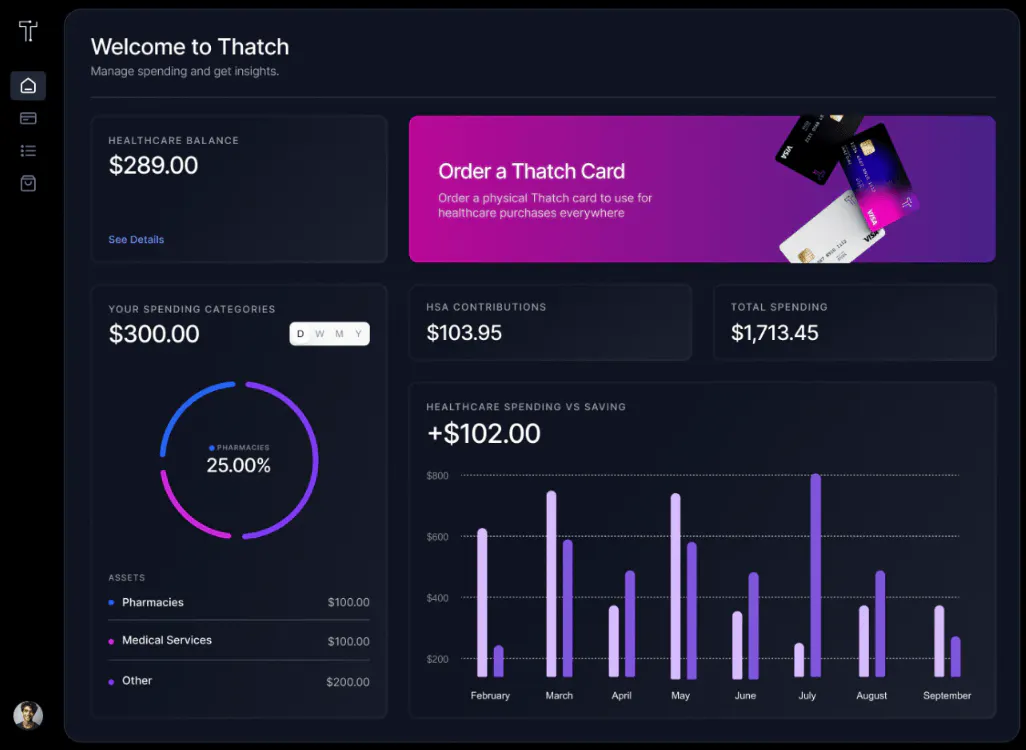

Employees receive their personal budget, which can be used for medical, dental, and vision insurance. Any remaining balance can be spent on qualified medical expenses using the Thatch debit card. That way, each employee can curate a unique plan for themselves.

Employees select their plans using Thatch's recommendations and the full list of available plans. They can also use the built-in AI support to ask questions and get additional context.

Source: Thatch

Once they select their plans, employees receive a summary of all their choices, highlighting any remaining balance that can be applied to expenses. That information is available on the employee dashboard, where they can also order their debit card, which is used to pay for qualified medical expenses online or in person.

On the back-end, Thatch deducts the total premium from the employer and then pays carriers. If the allowance doesn’t fully cover the premium, in instances where the employee has selected more expensive plans, the employer deducts the difference from the employee.

Source: Thatch

Broker Platform

Thatch also supports insurance brokers in administering ICHRA plans for their clients. The platform offers a suite of features designed to improve the process of setting up and managing ICHRA, enabling brokers to deliver personalized, flexible, and cost-effective health benefits to their portfolios of companies.

The broker platform includes instant quoting tools to estimate healthcare costs, automated billing and payouts to minimize administrative workload, and a preconfigured ICHRA setup process that allows brokers to launch new client accounts. The system also offers budget calculation tools that enable brokers to help employers set contribution levels across employee tiers.

Platform APIs

The majority of employer and broker platform functionality can also be provided as a set of APIs and embeddable widgets for other large companies looking to embed these features on their platforms rather than redirecting to the Thatch website. Thatch platform APIs also support QuickBooks to integrate ICHRA directly with existing SMB workflows. Thatch offers a similar pairing with ADP, which launched in December 2025.

Marketplace

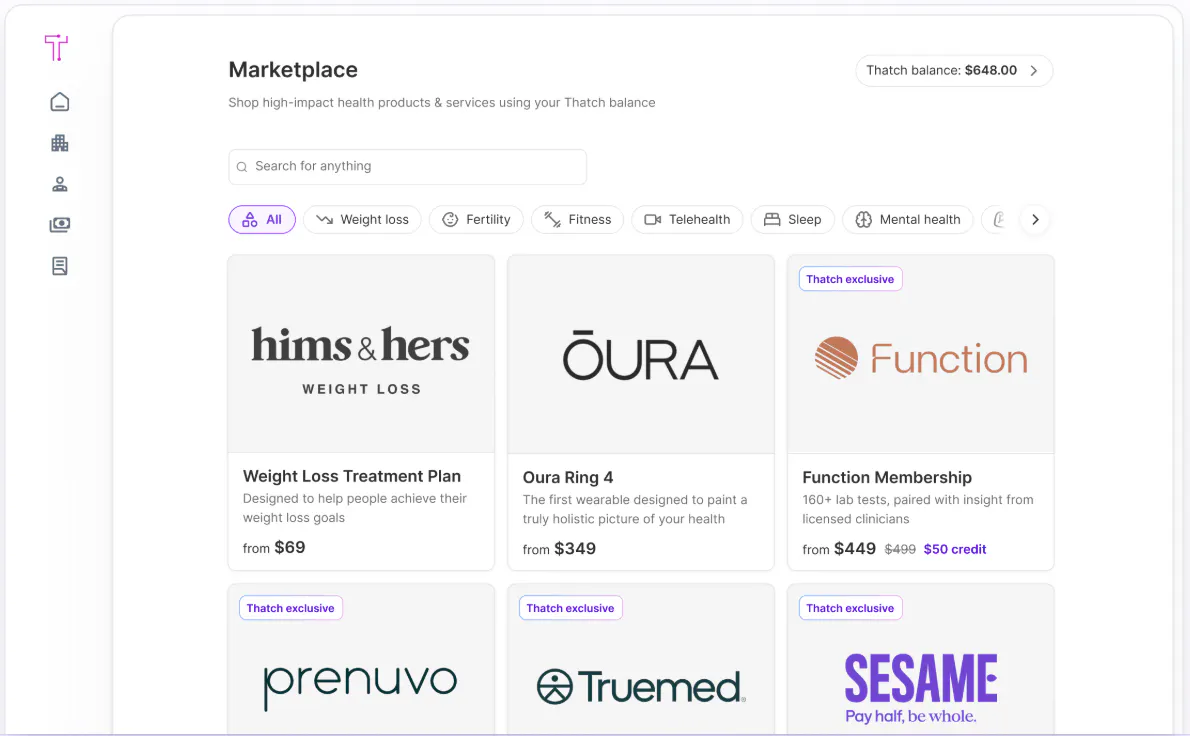

Around 50% of employees onboarded on Thatch carry a balance of around $250 per month after paying for their insurance, which accumulates with time. To facilitate spending that balance, Thatch built a curated marketplace for qualified medical expenses, where employees can choose from various services and products, including diagnostics, fertility care, therapy, telehealth, and functional medicine.

of employees onboarded on Thatch carry a balance of around $250 per month after paying for their insurance](https://images.prismic.io/contrary-research/aepHssBOoF08xQdH_image7.png?auto=format%2Ccompress&fit=max&w=1080)

Source: Thatch

The Marketplace features partnerships with leading health and wellness providers, offering exclusive member pricing on services such as whole-body MRI scans from Prenuvo, telehealth consultations via Sesame, personalized health tracking with Oura, comprehensive lab testing through Function Health, genomic testing via MyOme, as well as hundreds of other products and services by integrating with the TrueMed ecosystem.

Source: Thatch

Market

Customer

The Thatch product found initial resonance with early-stage, distributed tech companies across the US, which are often underserved by traditional group health plans and looking for flexible, cost-predictable benefits to cover employees spread across multiple states. While the company gained initial traction among SMBs, the Thatch platform is also built to support large organizations. These firms often have complex benefits requirements such as multi-state compliance, ACA reporting, integration with existing HRIS and payroll systems, and more robust employee support.

As of April 2026, Thatch’s customer base spans across industries and includes tech start-ups, mid-market trucking and solar installation firms, marketing agencies, and even dental clinics. It has also onboarded key insurance brokers such as Allstate, WTW, KBI, Marsh McLennan Agency, and ICHRA Shop. As of April 2025, Thatch had onboarded over 1K customers in the prior 18 months. Notable customers include Dave’s Hot Chicken, Jersey Mike’s, Fragment.dev, and Friends of Bonobos. To accelerate penetration into the enterprise segment, Thatch has also entered strategic partnerships with national large-group brokers such as AON and Mercer.

There are two primary challenges to scaling Thatch’s customer base. First, SMBs often require education and support, as many remain unaware of ICHRAs as a viable alternative to traditional group plans, with 72% of small-business leaders not familiar with ICHRAs as of May 2025. Second, broker adoption has been difficult, as ICHRAs disrupt the traditional business model: not only are commissions usually lower, but many ICHRA administrators also become the agent of record (AoR), limiting the broker’s long-term revenue.

Market Size

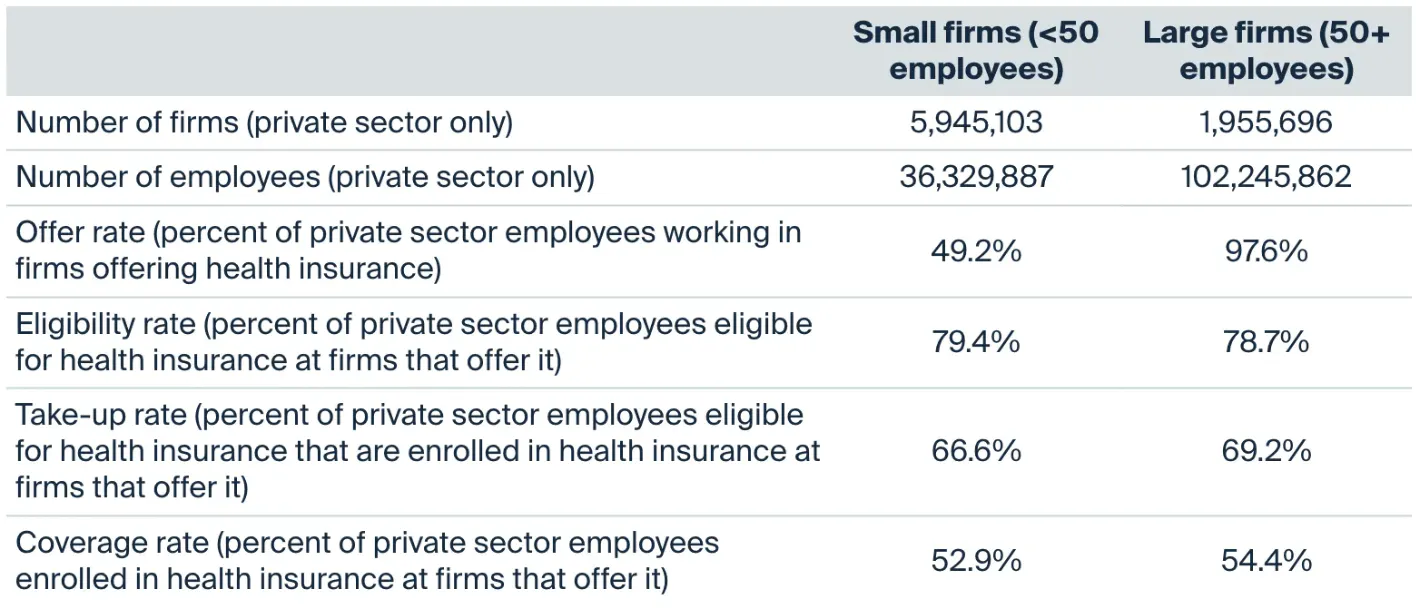

In 2023, there were close to 6 million small firms (fewer than 50 employees) in the US private sector, employing more than 36 million people. Only 49.2% of these employees worked at firms offering health insurance, and of that group, only 52.9% were covered by insurance, implying that only 26% of private sector employees at small firms were covered by health insurance.

Source: The Commonwealth Fund

ICHRA is increasingly serving as a first step into employer-sponsored health benefits. As of 2024, 83% of employers adopting ICHRA, or its forerunner, QSEHRA, had not previously offered health insurance. The remaining 17% transitioned from traditional group plans. Adoption has been especially strong among Applicable Large Employers (ALEs), who are mandated under the ACA to cover at least 95% of their full-time employees; this segment saw an 84% increase in ICHRA adoption in 2024. In total, around 5K firms offered ICHRA in 2024, representing 30% year-over-year growth, with an estimated 500K to 1 million individuals enrolled, including dependents.

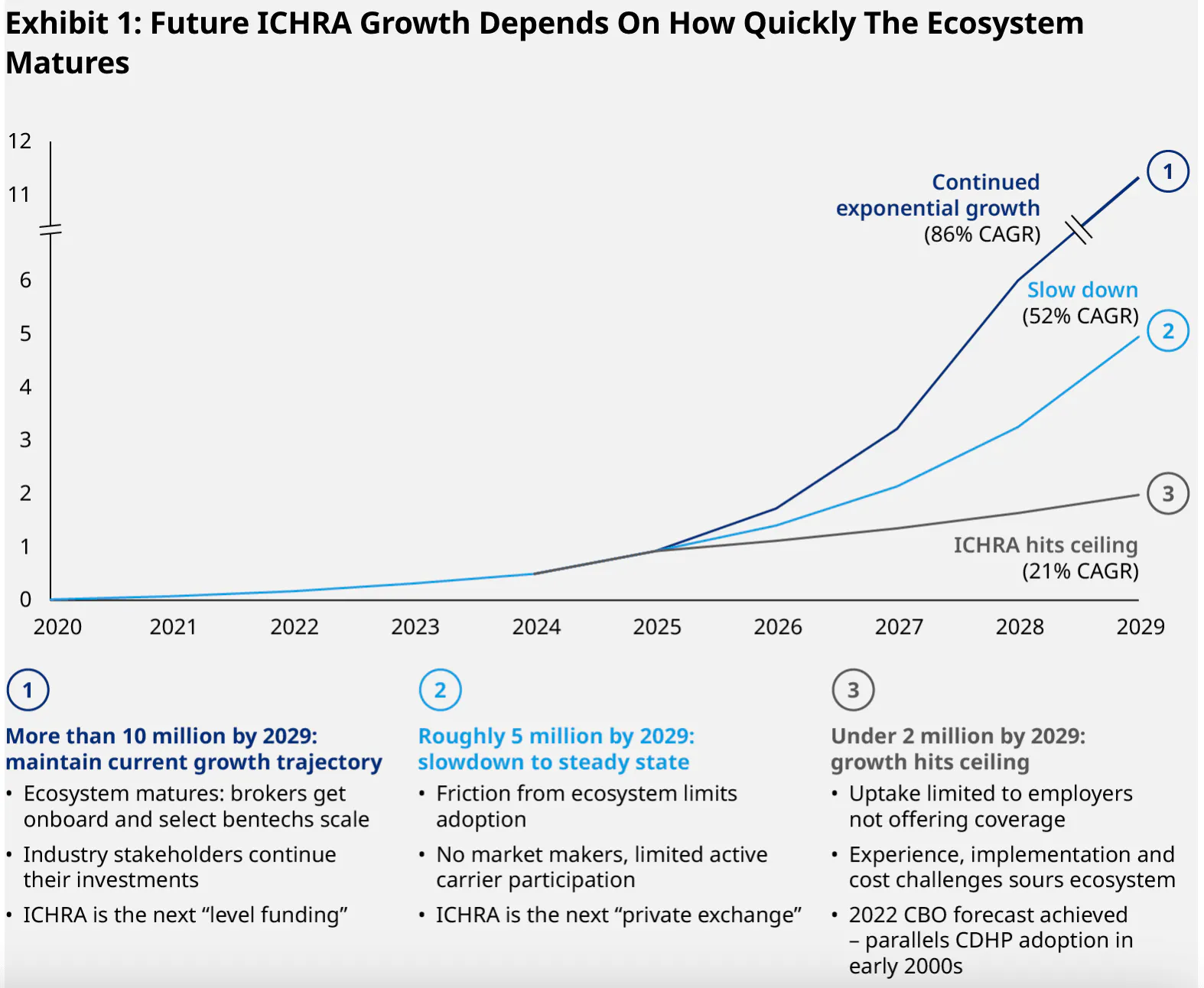

Given these industry dynamics, the long-term ICHRA target market includes millions of firms and tens of millions of employees. This spans both small businesses that have not traditionally offered insurance and private sector firms of any size seeking to lower costs, reduce administrative complexity, and offer employees more choice and control. As of 2024, market projections outline three potential growth scenarios for ICHRA adoption through the remainder of the decade:

Source: OliverWyman

Competition

Overview

The ICHRA administration market is varied, with employer needs and expectations differing significantly based on company size. Elements like distribution channels, support needs, technology infrastructure, and price sensitivity vary between small and large employers. Consequently, many ICHRA administrators primarily target one employer size segment, although most still engage with employers of varying sizes.

Focusing on the small employer market is relatively common among administrators, driven by higher conversion rates and unique compliance requirements. Concentrating solely on large employers has traditionally been more difficult due to lower ICHRA adoption and the influential role of brokers, which tend to serve clients across the size spectrum.

As mid-sized and large employers increasingly become aware of and adopt ICHRA, some administrators are broadening their focus to cover the full range of employer sizes. This trend highlights emerging opportunities while also introducing challenges in scaling solutions to accommodate employers' diverse needs.

Take Command

Take Command, founded in 2014, is a full-service ICHRA platform that originally launched as a QSEHRA (qualified small employer health reimbursement arrangement) provider. While its average client has about 15-20 employees, the company is seeing its fastest growth among mid-sized firms (50–500 employees) and also serves several clients with over 1K employees. Take Command retains agent of record (AoR) status for 100% of its enrollments, charging small employers (less than 50 employees) $20 per employee per month (PEPM) and mid-sized to large firms $30 or more.

In September 2023, the company raised $25 million in a Series B round led by Edison Partners, with participation from LiveOak Ventures and SJF Ventures. The round valued the company at $115 million and brought its total funding to $46.2 million. A key differentiator is its business model: unlike many competitors, it retains full AOR status while scaling across employer sizes.

Zizzl Health

Founded in 2016, Zizzl Health initially operated as a payroll and benefits agency before specializing in ICHRA administration. The company offers mid-sized employers an off-exchange, group-like health insurance experience and provides a white-labeled platform that allows brokers to retain their AoR status.

In May 2025, Zizzl Health secured $10 million in funding from Arthur Ventures. As of April 2026, the company has raised $26.5 million in total funding from Arthur Ventures, CSA Partners LLC, and others. A key differentiator for Zizzl Health is its broker-friendly approach. Unlike many competitors, it allows external brokers to maintain their AoR status by default, trading some commission for quicker adoption through established channels.

Gravie

Founded in 2013, Gravie stands out among ICHRA administrators by offering both a proprietary group health plan, called Comfort, and a flexible ICHRA platform, giving employers a broader set of benefits options. As of April 2026, the company has raised a total of $532.6 million in equity and debt financing from investors, including General Atlantic, Georgian, AVP, and Trinity Capital. In June 2025, Gravie raised $150 million from private equity investors, following a $40 million debt raise 12 months prior. Gravie differentiates itself by combining risk-bearing group plans with ICHRA administration, offering a level of vertical integration not typically found in the space.

Business Model

Overview

Typically, ICHRA administrators charge employers a per-employee-per-month (PEPM) fee, calculated based on the number of employees actually enrolled in the plan. This administrative fee compensates the administrator for managing plan logistics, ensuring compliance, and providing ongoing employee support.

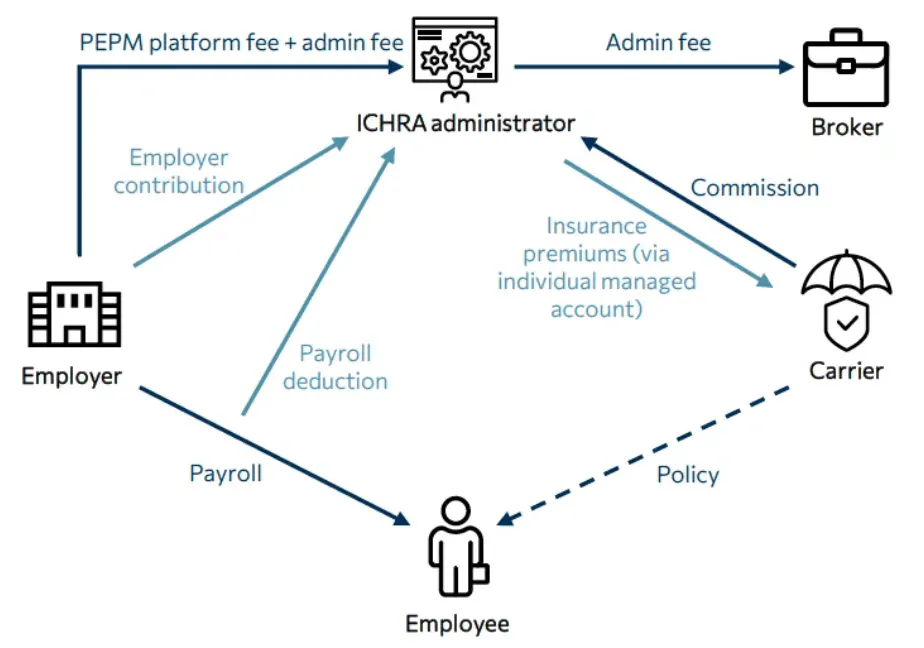

ICHRA administration companies generally hold insurance brokerage licenses across all 50 states, enabling them to facilitate individual health plan enrollments for all clients directly. Enrollment commissions from insurance carriers can be managed in one of two ways, depending on whether a third-party broker is involved in the client relationship. If an external broker handles the client relationship, that broker may act as the agent of record (AOR), directly collecting commissions from insurance carriers for individual enrollments. Alternatively, and more commonly, the ICHRA administrator itself becomes the AOR, directly receiving commissions from carriers and altogether simplifying the administrative process. Depending on the market, commissions range from $15 to $25 per employee per month.

When the ICHRA administrator acts as the AOR but a third-party broker initially facilitated the client acquisition, the broker is typically compensated through an additional PEPM administration or consulting fee charged directly to the employer. The ICHRA administrator collects this fee on the broker's behalf and passes it directly to them. This arrangement ensures brokers remain adequately compensated for their role in client acquisition, acknowledging that ongoing client support and administrative responsibilities primarily reside with the ICHRA administrator.

Source: Bailey & Company

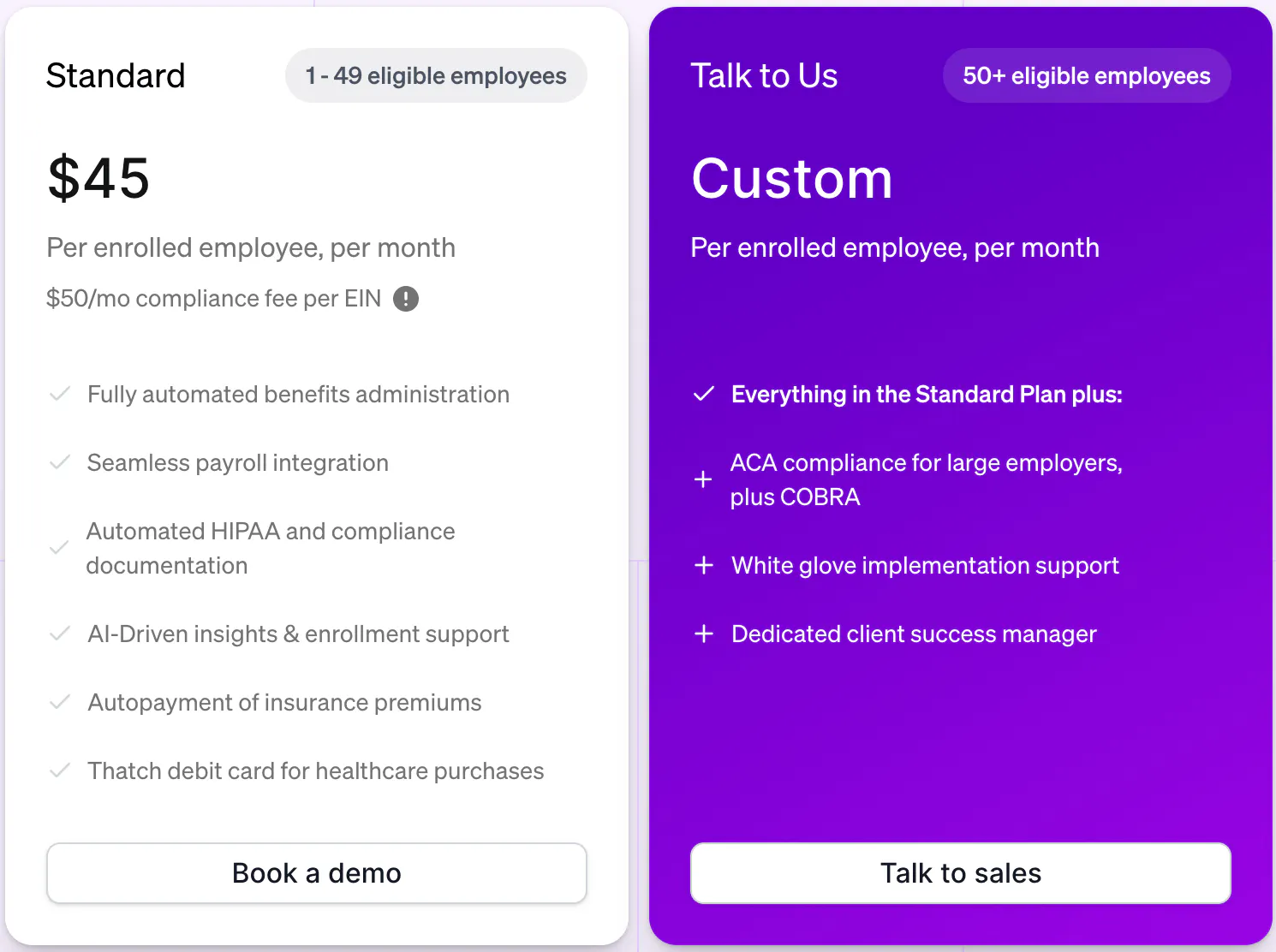

Thatch

Thatch charges employers a monthly subscription fee per employee and a monthly compliance fee per firm. For small firms with less than 50 employees, Thatch charges $45 per enrolled employee per month plus a $25 monthly compliance fee per firm. Firms with 50 employees or more get custom pricing depending on the total size of enrollment. Thatch also holds insurance brokerage licenses across all 50 states, allowing the company to retain AOR status whenever possible and generate revenue through commissions received from insurance carriers. These commissions result from directing new enrollments toward carriers, reinforcing Thatch’s role as both a benefits platform and a valuable distribution channel within the healthcare ecosystem.

Source: Thatch

Additionally, Thatch captures incremental revenue from interchange fees on card transactions. Employees utilize Thatch-issued benefits cards for qualified medical expenses, enabling Thatch to earn transaction-based interchange fees each time the card is used.

Thatch Marketplace operates a business model that aggregates demand from users with accumulating pre-tax healthcare balances, enabling it to negotiate preferential pricing with premium healthcare providers, such as securing $400 discounts on Prenuvo full-body MRI scans. This creates a dual-sided value proposition: users gain access to discounted, high-quality services using pre-tax dollars, while vendors benefit from a captive audience with constrained purchasing power that can only be spent on qualified medical expenses. As the orchestrator, Thatch monetizes this ecosystem by taking a revenue share on each transaction.

Traction

The ICHRA market grew by 29% from 2023 to 2024, with an estimated 4K firms offering ICHRAs in 2024 and 500K to 1 million employees enrolled. Applicable Large Employers offering ICHRA grew by 84% in that period. At the same time, 89% of employers aware of ICHRA are considering offering them within the next three years.

As of April 2025, Thatch had onboarded over 1K customers in the prior 18 months, and the company’s year-over-year revenue had grown eightfold. In November 2024, Thatch launched an integration with QuickBooks, a leading payroll provider, to enable small businesses to integrate with Thatch. A similar integration with ADP launched in December 2025, targeting ADP’s RUN user base of over 900K companies. Both of these partnerships expose Thatch to a large pool of SMBs and aim to support its future growth. Thatch's 2025 revenue growth was estimated to be 4x in October 2025.

In April 2026, Thatch acquired former competitor Venteur at an undisclosed price. Founded in 2021, Venteur provided AI-powered health insurance plan curation and year-round concierge support. It primarily targeted large employers (70% of its customers) but also served small groups through a self-serve platform priced at $20 per employee per month (PEPM). In April 2025, Venteur raised a $20 million Series A led by Informed Ventures and American Family Ventures, with a total of $27.7 million in external funding prior to the acquisition. Thatch integrated all of Venteur’s existing customers as part of the deal.

Valuation

In April 2025, Thatch raised a $40 million Series B led by Index Ventures with participation from existing investors Andreessen Horowitz (a16z), General Catalyst, and others, as well as new investor ADP Ventures. While Thatch declined to reveal its valuation during that round, co-founder Stevenson indicated that it was about three times higher than its Series A, when the firm raised $38 million from Index Ventures, General Catalyst, Andreessen Horowitz, and others, at a $135 million valuation. This implies a Series B valuation of around $400 million.

In February 2023, Thatch came out of stealth with a $5.6 million seed round, co-led by Andreessen Horowitz and Google Ventures (GV), with participation from Lux Capital, Quiet Capital, Not Boring Capital, and BrightEdge (the impact investment arm of the American Cancer Society). As of April 2026, Thatch has raised $84 million in equity funding since inception (including a $400K pre-seed).

Key Opportunities

A Growing ICHRA Market

As of April 2026, there were close to 136 million private sector employees in the US, and only 500K to 1 million of them were enrolled in an ICHRA plan. As many as 89% of benefits decision-makers who don't currently offer ICHRAs are considering ICHRAs for their employees over the next three years. Others are looking further out, with 87% of surveyed respondents agreeing that ICHRA could be a long-term fit for their company. The ICHRA market represents a large opportunity with structural tailwinds. Thatch has the opportunity to capture a share of this growing market by offering a differentiated product, owning the category education narrative, clarifying the value proposition of ICHRAs, and accelerating adoption.

Data Moat

One of Thatch’s long-term strategic moats lies in its ability to aggregate and operationalize benefits data at scale. As more employers onboard the platform and more employees enroll in individualized health plans and spend remaining funds on qualified medical expenses, Thatch builds a growing corpus of benefits data, covering demographics, preferences, conditions, spending behavior, and outcomes. Over time, this dataset enables Thatch to shift from a benefits orchestrator to a benefits advisor. In addition to its existing package recommendations, the company could intelligently design condition-specific plan recommendations (e.g., chronic care bundles), offer proactive suggestions for ancillary products, surface value-for-money insights, or build its own proprietary healthcare solutions.

Key Risks

Competition

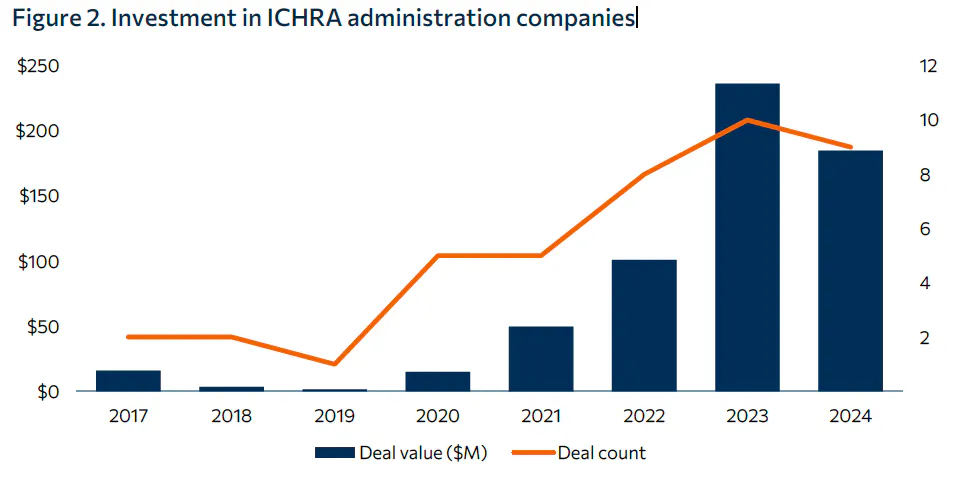

Thatch faces growing competition as investment in ICHRA administration companies accelerates. Deal value in the space has been increasing consistently since the official launch of ICHRA in 2020. In 2023 and 2024, there were 19 funding deals for ICHRA administration companies, raising more than $400 million in total, marking a sharp increase in both investor interest and market entrants. Additionally, established HR platforms (e.g., Rippling) or large health insurers, which already have distribution scale, infrastructure, and customer trust, may replicate ICHRA capabilities. For example, in 2024, Oscar Health announced its intention to enter the ICHRA market and offer a proprietary solution. If Thatch does not scale quickly enough or carve out a defensible niche, it may struggle to compete against these giants as they vertically integrate downstream.

Source: Bailey & Company

Slow Adoption Curve Despite Policy Tailwinds

Several major US health insurance reforms (like HSAs, Medicare Advantage, and the ACA) faced long, uneven adoption curves despite strong government backing. In each case, mass uptake took nearly a decade because widespread adoption required multiple stakeholders (carriers, brokers, regulators, and consumers) to move in sync. Progress stalled until ecosystem players built compatible offerings, adjusted rules, or fixed technical barriers. ICHRA may follow a similar path. While the policy is structurally sound, Thatch faces the real risk that adoption will be slower than venture timelines allow, especially given annual enrollment windows and the need to onboard both employers and distribution partners. Without faster channel coordination, cash needs could outpace growth.

Rising Premiums Could Undermine ICHRA’s Cost Advantage

ICHRA adoption hinges on individual-market health plans remaining more affordable than comparable small-group coverage. This price gap allows employers to offer benefits at a lower cost while giving employees more flexibility. However, that cost advantage is fragile. A sharp rise in individual-market premiums, or a narrowing of the pricing gap, could quickly erode ICHRA’s value proposition. Employers may see little reason to switch if individual plans become more expensive than group alternatives.

A key variable is federal policy. In particular, the Affordable Care Act’s premium subsidies (APTCs) are critical to keeping individual-market plans affordable. These enhanced subsidies expired in January 2026, causing premiums to increase, especially in less competitive state exchanges. This exemplifies a significant macro risk for Thatch: policies shift outside the company’s control could suddenly make ICHRA financially unattractive to employers, limiting near-term growth and threatening long-term viability in certain markets.

Summary

The US employer-sponsored health benefits market is undergoing a structural shift as businesses, especially small and mid-sized firms, seek alternatives to the cost and complexity of traditional group plans. ICHRA (Individual Coverage Health Reimbursement Arrangement), introduced in 2020, is emerging as a flexible solution. It allows employers to reimburse employees tax-free for individual-market health insurance premiums, converting rising healthcare costs into a defined-contribution model. Early adoption data is promising: over 80% of ICHRA-adopting firms in 2024 offered health insurance for the first time, and Applicable Large Employers (ALEs) saw 84% year-over-year growth in adoption. With only 500K to 1 million current enrollees and tens of millions of US employees still uncovered, the ICHRA market remains in the early innings, with strong regulatory tailwinds but a multi-year adoption curve ahead.

Thatch is a fintech-forward ICHRA platform built to serve this opportunity. Focused initially on SMBs, Thatch offers low-friction onboarding, payroll integrations, and employee-first tooling, positioning it as both a benefits administrator and a distribution layer for the individual health insurance market. With 8x revenue growth in the past year, integrations with QuickBooks and ADP, and a growing marketplace for ancillary healthcare spending, Thatch aims to build network effects and a data moat. Key risks include growing competition both from incumbents and new players, policy volatility around ACA subsidies, and the potential for ICHRA adoption to lag venture expectations due to stakeholder coordination challenges. The key question remains whether Thatch can scale fast enough, build distribution and data moats, and maintain its cost advantage to become the defining platform for the next wave of employer-sponsored healthcare.

*Contrary is an investor in Ramp through one or more affiliates.