Thesis

At the end of 2024, ~11.5K satellites were operating in Earth orbit compared to just ~3.4K in 2020. This pace of satellite deployment is expected to increase, as global satellite operators have announced plans to launch up to 70K Low Earth Orbit (LEO) satellites between 2025 and 2031. LEO satellites must be replaced every five years, which creates recurring demand for launch services even if the total number of satellites in orbit plateaus.

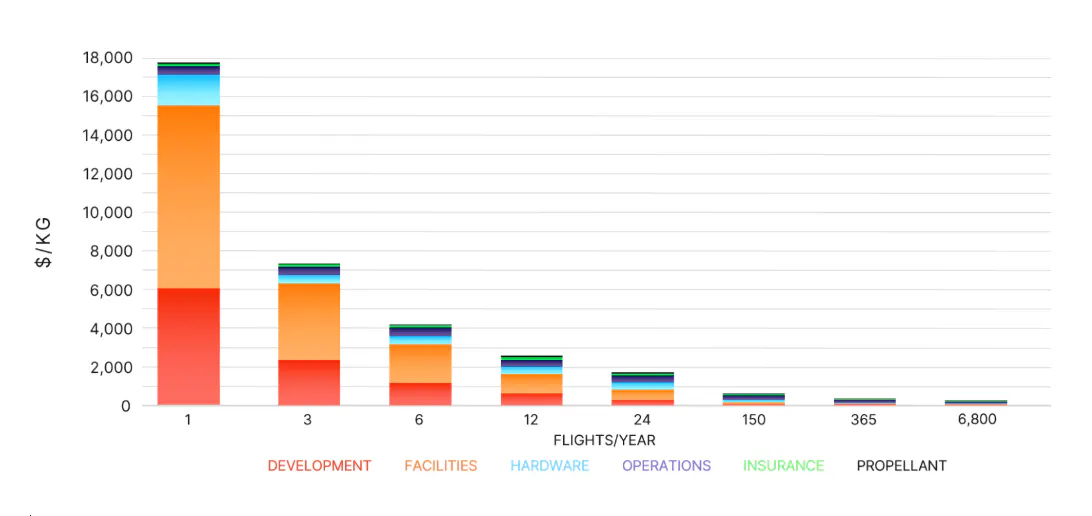

Meeting launch demand at this scale relies on low-cost space launch services. NASA’s space shuttles, which were active from 1981 to 2011, cost nearly $30K per pound of payload to reach LEO. After SpaceX became the first company to recover a reusable orbital-class rocket booster in December 2015, it emerged as the leading force in the global launch industry. In 2022, SpaceX charged its customers $1.2K per pound of payload launched on the company’s partially reusable Falcon 9 rocket. SpaceX set a goal in 2017 to achieve a 24-hour first-stage reuse turnaround by 2018, but as of June 2026, the company has not met this target.

Source: Stoke Space

Stoke Space is an aerospace manufacturer building medium-lift orbital rockets designed to lower the cost of spaceflight and enable rapid, on-demand orbital deliveries. The company is built on the belief that the limiting factor in reducing launch costs for partially reusable rockets like the Falcon 9 is rapid verification and reinstallation of the second stage. By designing a fully reusable rocket, Stoke Space aims to achieve a 24-hour turnaround time for reuse by designing first- and second-stage components that can be reused with minimal inspections or refurbishments between launches. This is intended to allow Stoke Space to focus turnaround time on less intensive tasks like re-stacking its rocket, reloading payload, and refueling before launch and amortize fixed costs, including factories, test facilities, and launch complexes, across many flights.

Founding Story

Stoke Space was founded in 2019 by Andy Lapsa (CEO) and Tom Feldman (CTO). Lapsa and Feldman met while working at Blue Origin. Before starting Stoke Space, Lapsa completed his PhD in aerospace engineering at the University of Michigan before working at Blue Origin for a decade, where he developed the company's propulsion systems. Andy was one of Blue Origin’s three original employees who developed the company’s BE-4 rocket engine before leading Blue Origin’s BE-3 and BE-3U engine programs. During this time, Feldman was working as a propulsion design engineer on the BE-4 engine's oxidizer pump and thrust chamber, having spent six years at Blue Origin.

Lapsa felt that, even though rocket companies like Blue Origin were focused on partial reusability (reusing only the first stage), full, rapid reusability was necessary to achieve optimal unit economics. The space landscape at the time included ~150 rocket startups, and Lapsa perceived “a lot of noise in the industry”. Lapsa began discussing full reusability with Feldman, initially without intending to start a company. After realizing that no company was successfully addressing this problem, the two decided to do so themselves.

After leaving Blue Origin in fall 2019, Lapsa and Feldman began working in Feldman’s basement to conduct in-depth technical and economic analysis of full reusability. At the time, Feldman had a three-month-old baby while Lapsa was raising a family. Given the technical and personal risks, the co-founders decided to commit six months to gaining traction before reevaluating whether to continue working on the company. In May 2020, Stoke Space received a $225K SBIR Phase I grant from the National Science Foundation to develop integrated propulsion systems for reusable rocket upper stages. Using that initial funding, the team built a prototype for a second-stage engine injector within a few months in a shipping container in Feldman's backyard. Stoke Space later joined Y-Combinator’s Winter 2021 batch.

Product

Nova

Source: Stoke Space

Stoke Space’s flagship product is its Nova rocket. Nova, built with 97% recycled stainless steel, can accommodate 3K kilograms to LEO in its fully reusable configuration. The rocket operates in the medium-lift market, defined by rockets capable of delivering 2K to 20K kilograms of payload to LEO. Stoke Space expects Nova to reduce launch costs by 20x compared to traditional launch vehicles. Nova is built for 100 launches, whereas the most SpaceX’s Falcon 9 booster has been reused was 34 times as of March 2026, and Blue Origin’s New Glenn booster is designed to be reused at least 25 times.

Nova’s first stage is powered by seven Zenith full-flow staged combustion (FFSC) engines. Each engine is capable of producing over 100K pounds-force of thrust. The reusable upper stage features a cooled metallic reentry heat shield with an integrated modular liquid hydrogen and liquid oxygen rocket engine. This fuel combination allows Stoke Space to access higher-energy orbits, such as trans-lunar injection and escape trajectories, that other medium-lift rockets generally cannot reach.

Stoke Space’s cooled metallic heat shield ensures the rocket can be rapidly reused, whereas heat shields made from ceramic tiles or ablative coatings require additional time to replace these materials after every launch. The upper stage features 24 thruster nozzles that line the circumference of the bottom of the second stage. Stoke Space completed a hopper test in September 2023 that involved flying the second stage to an altitude of 30 feet for 15 seconds before landing at a planned zone.

Boltline

Source: Boltline

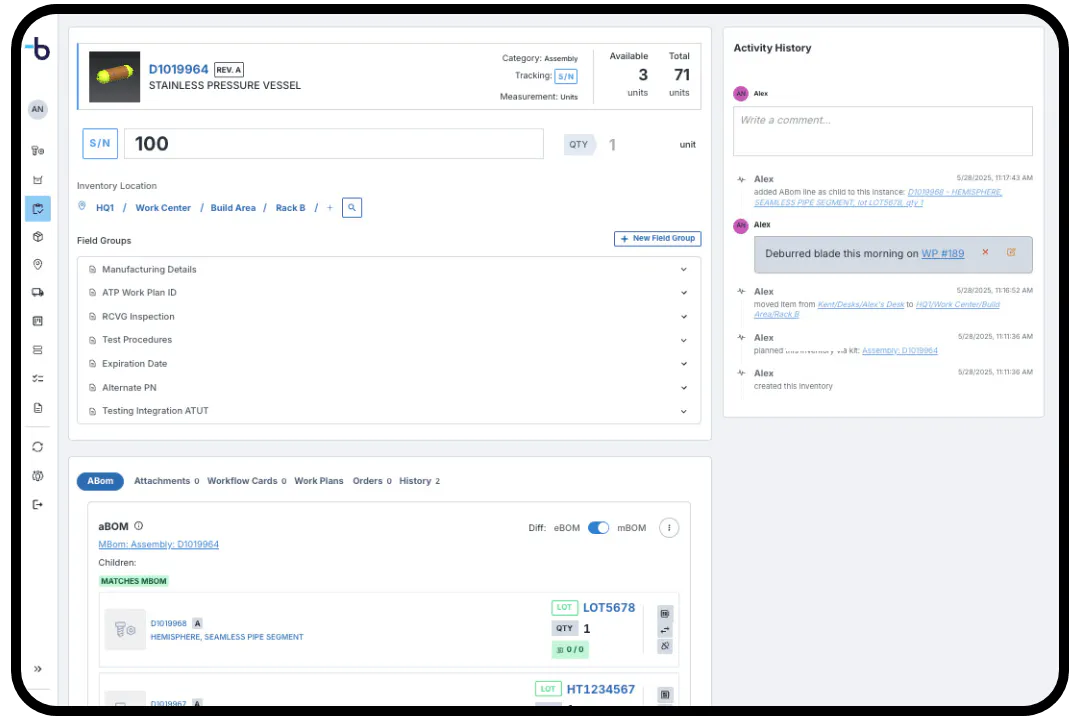

While Stoke Space was in early prototyping, it struggled to use off-the-shelf software tools that could keep up with the company’s iteration speed. To address this challenge, Stoke Space developed an internal unified system to track the design, testing, and integration of parts. It later released this software product to the public as Fusion, later rebranding it as Boltline. Stoke Space reported that it doubled Boltline's revenue in the first half of 2025. Some of Boltline's aerospace customers include ispace and Intuitive Machines. Internally, Boltline has also reduced production inefficiencies at Stoke Space.

Market

Customer

Stoke Space primarily targets commercial satellite operators and the US government. Medium-lift launch vehicles like Nova are particularly suited for satellite deployment where customers require a balance between payload capacity and cost-effectiveness. The commercial satellite market is led by several satellite operators, including Amazon's Leo, Eutelsat's OneWeb, Telesat's Lightspeed, and newer entrants such as AST SpaceMobile. Satellite operators are required by FCC regulations to deorbit their satellites in LEO after five years to reduce the risk of accumulating space debris. Thus, launch providers like Stoke Space benefit from ongoing demand for launch services as operators must consistently replace their satellite constellations.

Stoke Space was selected for the US Space Force's National Security Space Launch Phase 3 Lane 1 program in March 2025, allowing the company to compete for up to $5.6 billion in government space launch contracts against SpaceX, Blue Origin, ULA, and Rocket Lab. The Lane 1 program allows the government to promote competition in the space launch industry by offering its more risk-tolerant payloads, while a separate Lane 2 program is reserved for launch providers with high reliability. Government demand for space launch services is emerging further through the Golden Dome, a plan that involves a constellation of thousands of LEO satellites to track and intercept potential missile attacks.

Market Size

The global space economy reached $613 billion in 2024 and is on track to exceed $1.8 trillion by 2035. Within this broader economy, the global launch services market was valued at $18.2 billion in 2025 and is expected to reach $45.9 billion by 2034 at a growth rate of ~10.8%. As of June 2026, the US leads the world in launch services, holding ~65% of the global launch market share.

Split by launch vehicle type (small, medium, and large-lift rockets), medium-lift launch vehicles held roughly 56.6% of the launch market share in 2024, with demand largely driven by commercial satellites. Global satellite operators have submitted or announced plans for 70K LEO satellites, scheduled to launch between 2025 and 2031. Because LEO satellites have a much smaller field of view compared to higher-orbit satellites, they are often deployed in larger numbers as satellite constellations. SpaceX pioneered the first mega-constellation with the launch of 60 Starlink satellites in 2019.

On the government side, launch capacity has increasingly become a national security priority. In a December 2025 executive order, the White House directed federal agencies to pursue more cost-effective launch and exploration architectures. Much of this urgency is driven by competition with China, which is second to the United States in orbital launch attempts. China’s three largest satellite operators plan to launch more than 10K satellites between 2025 and 2031, a significant expansion from the ~1.4K satellites the country had in orbit at the end of 2025.

Orbital data centers are another emerging market for the space launch industry. Google, which is developing satellites carrying its Tensor Processing Units, believes that launch costs must drop to $200 per kilogram for orbital data centers to be profitable. However, the Nova rocket’s limited payload capacity compared to a larger launch vehicle like Starship limits Stoke Space’s ability to compete in this market.

Competition

Competitive Landscape

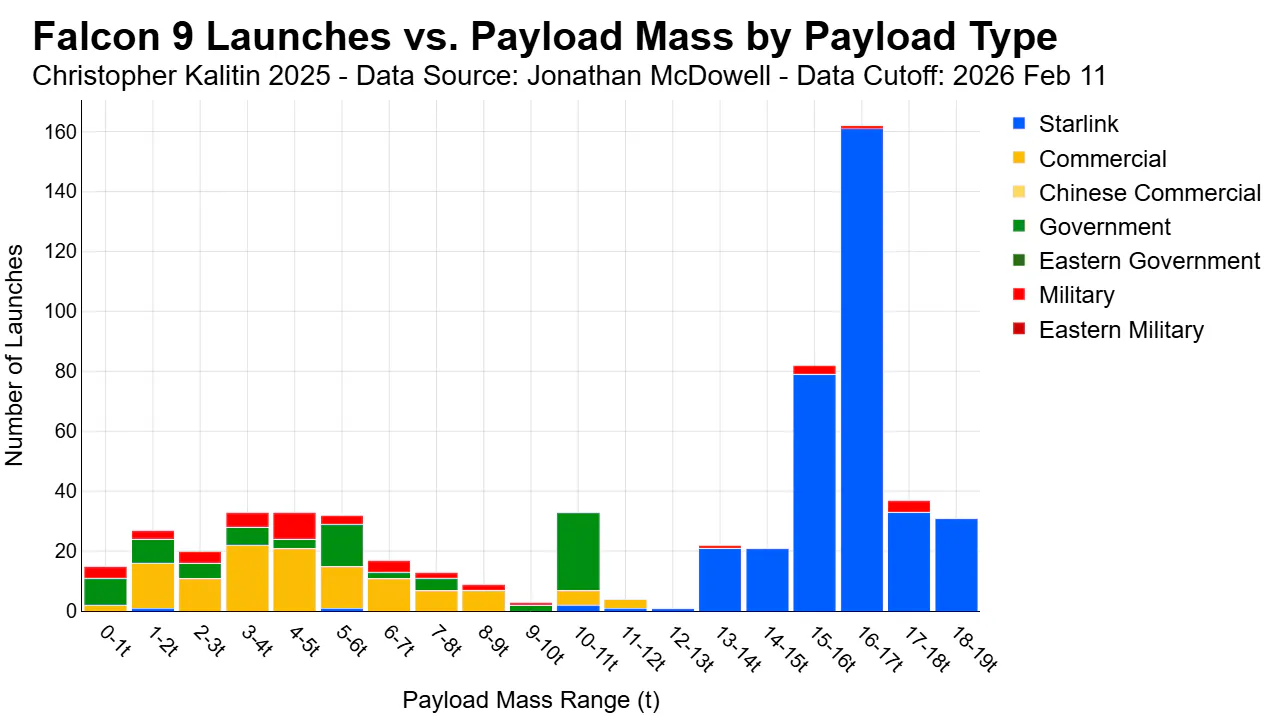

SpaceX’s Falcon 9 rocket accounted for 85% of all rocket launches in the United States in 2025, making it the dominant player in the space launch industry. About 74% of SpaceX’s launches in 2025 were for the company’s Starlink constellation, while the remainder were for commercial and government customers. Despite SpaceX’s dominance, demand for commercial launch capacity is expected to outpace launch availability, excluding potential demand from other launch opportunities such as orbital data centers.

Source: Christopher Kalitin Blog

Falcon 9 launches to LEO can carry 22.8K kilograms of payload. On average, SpaceX’s launches carry about 16.9K kilograms of payload. However, LEO launches for commercial customers, which often require specific orbits and launch parameters, carry just 3.4K kilograms of payload, using only 14.9% of the Falcon 9’s total launch capacity. Stoke Space’s launch vehicle, which can lift 3K kilograms of payload to LEO, targets commercial customers with a dedicated launch vehicle that can match payload needs without creating significant unused capacity. If successful, Stoke Space’s Nova rocket will operate with a LEO payload capacity between the 22.8K kilograms of SpaceX’s Falcon 9 and the 300 kilograms of smaller rockets like Rocket Lab’s Electron vehicle.

SpaceX

Founded in 2002 by Elon Musk, SpaceX is the pioneering company in the commercial space launch industry. SpaceX developed two partially reusable launch vehicles (the Falcon 9 and Falcon Heavy rockets) and the fully reusable Starship. SpaceX is the only other space company pursuing full reusability with Starship, although Starship is in a different launch-weight class. The majority of the company’s revenue comes from Starlink.

SpaceX flew Falcon 9 165 times in 2025, accounting for about 85% of US orbital launches in that year. Despite its substantial market share, the Falcon 9 remains only partially reusable, which imposes a cost floor. The first stage, which accounts for about 60% of the total rocket cost, is recovered and reflown, while the second stage, which accounts for 20% of the total cost, is expended and replaced on every mission.

A December 2025 secondary tender offer valued SpaceX at ~$800 billion, with a planned IPO in 2026. In February 2026, SpaceX acquired Musk’s artificial intelligence company, xAI, to build orbital data centers as a more efficient alternative to terrestrial data centers. The acquisition valued SpaceX at $1.25 trillion. The company exceeded $2 trillion in market cap when it went public in June 2026, raising $75 billion, and was trading at $1.8 trillion as of July 2026.

Blue Origin

Founded in 2000 by Jeff Bezos, Blue Origin operates the suborbital New Shepard rocket and the heavy-lift New Glenn rocket. The company is also competing with SpaceX to develop its Blue Moon lunar lander. While the company suffered years of delays, it achieved its first orbital launch with New Glenn in January 2025. Blue Origin is targeting a near-term rate of 12 launches per year and plans to reach 100 launches per year by 2029.

Despite its progress in developing reusable rockets, Blue Origin has faced setbacks. In April 2026, the company failed to deliver a satellite for AST Spacemobile to LEO. In May 2026, the company’s New Glenn rocket exploded on its launchpad, potentially delaying its future missions. Since its founding, Blue Origin has been funded entirely by Bezos, who has invested over $14 billion into the company as of January 2025. Blue Origin is expected to incur $4.8 billion in costs in 2026. Facing these challenges, Blue Origin’s CEO, Dave Limp, has acknowledged that meeting the company’s target of 100 New Glenn launches per year by 2029 would require additional external capital.

Rocket Lab

Founded in 2006, Rocket Lab is a space launch company focused on small and medium-class rockets, primarily for the nanosatellite and microsatellite markets. The company operates its small-lift rocket, Electron, which can carry up to 300 kilograms of payload to LEO, and is developing its medium-lift rocket, Neutron, which can carry up to 13K kilograms of payload to LEO. Rocket Lab plans to launch its maiden flight with Neutron in late 2026. Rocket Lab is the first rocket company to 3D-print its rocket engines, enabling it to manufacture more rockets at scale. As of June 2026, Rocket Lab has completed 87 successful launches with its Electron rocket. In the first quarter of 2026, the company booked more launches than it did in all of 2025. Rocket Lab has a market cap of $49.2 billion as of July 2026.

Relativity Space

Founded in 2015, Relativity Space designs rockets with 3D-printed components. The company operates the Terran R, a partially reusable rocket that can lift 23.5K kilograms of payload to LEO with a first stage that can be reused at least 20 times. The company’s first rocket was the Terran 1, which was 85% 3D-printed by mass, including its engines and propellant tanks. Terran 1 launched on its maiden flight but failed to reach orbit after an engine appeared to lose ignition. Following this, Relativity Space retired the program and pivoted to Terran R, which relies less on 3D-printed components.

Relativity Space originally designed the Terran R to be fully reusable, but switched to partial reusability to accelerate the rocket’s path to the commercial launch market. The company is planning its first launch of Terran R for late 2026. In March 2025, Eric Schmidt, the former CEO of Google, took over Relativity Space after making a significant investment in the company. As of June 2026, Relativity Space has raised $1.4 billion in funding, with a $650 million Series E in June 2021.

Firefly Aerospace

Founded in 2017, Firefly Aerospace provides launch solutions through its Alpha and Eclipse launch vehicles. Alpha is a small-lift rocket capable of carrying over 1K kilograms of payload to LEO, while Eclipse is a medium-lift rocket capable of lifting over 16K kilograms of payload to LEO. In March 2026, Firefly Aerospace completed its seventh launch with Alpha. Firefly Aerospace plans to achieve its first launch with Eclipse in 2027. In March 2025, Firefly Aerospace made the first commercial moon landing with its Blue Ghost lunar lander. Following this, the company went public in August 2025 with a valuation exceeding $6 billion. As of July 2026, Firefly Aerospace had a market cap of $3.6 billion.

Business Model

Stoke Space plans to generate revenue through dedicated commercial launches, rideshare missions, and government launch contracts. Lapsa claims that at a high reuse rate, Stoke Space could achieve unit costs of a few hundred dollars per kilogram rather than a few thousand, as reflected in incumbent launch providers' pricing.

Stoke Space aims to accomplish this by spreading the fixed costs of space launch over a large number of launches. The company’s rocket design, in particular its second stage, is designed to minimize the refurbishments and diagnostics required to ensure that the rocket can be reused. Stoke Space also operates Boltline as a separate subscription SaaS product. The platform is sold to hardware engineering teams across aerospace, biotech, and advanced manufacturing.

Traction

Stoke Space has made significant progress on its technology development. In September 2023, Stoke Space completed a successful vertical takeoff and vertical landing developmental test flight of its Hopper2 rocket, which is used in Nova’s fully reusable second stage. Following this, Stoke Space conducted its first successful hotfire test for its first-stage rocket engine in June 2024. Stoke Space completed the design and manufacturing of this engine in just 18 months.

In March 2023, Stoke Space was allocated Launch Complex 14 at Cape Canaveral Space Force Station. The site was previously designated as a National Historic Landmark. In October 2024, Stoke Space secured a license to develop and operate the launch site. It broke ground with heavy machinery on site less than 24 hours after obtaining the license. Its developments and renovations on the site included a Horizontal Integration Facility, a launch mount, an umbilical support structure, a flame trench and diverter, and propellant systems. The company expects the facility to be fully activated by early 2026, with the company’s first launch expected later in the year. In January 2024, Stoke Space also established a new 168K-square-foot production and operations headquarters.

Stoke Space has achieved customer validation from both government and commercial customers. In March 2025, the United States Space Force chose Stoke Space to participate in the National Security Space Launch Phase 3 Lane 1 program, allowing the company to compete for up to $5.6 billion in national security launch contracts. Stoke Space is one of five companies in this program, among competitors such as Rocket Lab, Blue Origin, SpaceX, and United Launch Alliance. Outside of government contracts, Stoke Space also has a manifest of commercial launch contracts. For example, Celestis, a space burial company, chose Stoke Space as its launch provider to send cremated remains and DNA samples into a permanent heliocentric orbit.

Valuation

In February 2026, Stoke Space raised $350 million in an extension of its $510 million Series D round from October 2025, valuing the company at approximately $2 billion and bringing its total funding to $1.4 billion. This round was led by Thomas Tull's US Innovative Technology Fund (USIT), with other investors including 776, Breakthrough Energy, Glade Brook Capital, Industrious Ventures, NFX, and more. Stoke Space planned to use its Series D funding to expand production capacity for its Nova launch vehicle and complete construction of its launch site at Cape Canaveral.

Key Opportunities

Growing Demand from Commercial Launch Customers

Demand for commercial launches is outpacing launch supply. Global satellite operators have submitted or announced 70K satellite plans for LEO, due to launch between 2025 and 2031, roughly six times as many satellites as were in orbit at the end of 2024. Jarrod McLachlan, director of rideshare sales at SpaceX, stated in 2023 that the company was seeing significant demand ƒor launches ahead in 2024 and even 2025.

Despite this, SpaceX prioritizes launches that support SpaceX’s internal capabilities. In 2025, 74% of SpaceX’s Falcon 9 launches were for Starlink. Lapsa describes how commercial customers are willing to pay more than what incumbent launch providers like SpaceX charge to receive launch availability. For instance, Rocket Lab’s Electron rocket is priced at about $25K per kilogram of payload but offers customers mission-specific orbital insertion and eliminates wait times.

Government Support

The White House’s Executive Order 14335 directs federal agencies to reform regulatory barriers in several key areas, including commercial launch and reentry, spaceport infrastructure, and the authorization of novel space activities. For example, the Executive Order removes duplicative safety reviews and cuts environmental reviews. Stoke Space's NSSL Phase 3 Lane 1 award positions the company to compete for up to $5.6 billion in national security launch contracts, including those that relate to the Golden Dome missile defense architecture. A Congressional Budget Office analysis projects that keeping 7.8K active Space-Based Interceptors in LEO would require ~30K satellites.

Downmass as an Untapped Market

Stoke Space defined downmass as one of its technology applications in its Series D press release. The Andromeda 2 (Stoke Space’s upper-stage engine) features improved downmass capacity compared to its first iteration. In the downmass market, SpaceX’s Dragon spacecraft is the only vehicle capable of returning cargo to Earth intact. Downmass capabilities allow for recovery of high-value goods manufactured or tested in space, such as advanced materials, semiconductors, and pharmaceuticals. In the pharmaceutical industry, space companies could earn between $2.8 and $4.2 billion in revenue by processing drugs in orbit. For certain drugs, even a kilogram of Active Pharmaceutical Ingredient is worth millions in revenues.

Key Risks

Full Reusability Remains Unproven

Stoke Space is pursuing a phased approach to conducting rocket launches. In the first phase, Stoke Space plans to launch the Nova rocket without recovering either stage at a low initial cadence. In the second phase, the company will test its fully reusable rocket following a supplemental environmental analysis. This is not an unusual approach, as SpaceX similarly achieved its first non-recovery launch in June 2010 and completed its first booster landing five years later in December 2015. However, Stoke Space has not announced when it expects to begin full reusability testing.

Competition in Full Reusability from SpaceX’s Starship

SpaceX’s Starship rocket is designed as a fully reusable heavy-lift launch vehicle, capable of carrying over 100 metric tons of cargo. Starship’s full reusability is expected to lower launch costs to $1.6K per kilogram, with further improvements potentially bringing costs down to below $150 per kilogram. To capitalize on Starship’s launch capabilities, SpaceX designed new V3 Starlink satellites, which were announced in October 2025. With 60 Terabits of downlink capacity, V3 Starlink satellites have more than 20 times the capacity of SpaceX’s previous V2 satellites. Starship can carry 60 V3 Starlink satellites per launch, each weighing 2K kilograms. If SpaceX’s vertically integrated business model succeeds, Starlink could worsen competitive dynamics for satellite rivals that serve as potential customers for SpaceX.

One mitigating factor is that SpaceX’s Starship and Stoke Space’s Nova are in different rocket classes and serve different purposes. SpaceX’s economics work with large payloads like Starlink V3 constellations. However, satellite operators with smaller-scale payloads often require specific launch parameters, making a Starship rideshare unfeasible. Stoke Space’s Nova could offer additional flexibility, as the rocket would be capable of flying more consistently with a cooled heat shield instead of heat tiles that require inspection after every flight. Furthermore, despite Starship’s potential unit economics, Lapsa believes that the rocket’s success would move the industry forward and prove complementary to Stoke Space, as Nova’s medium-lift rocket would serve distinct mission types rather than compete directly.

Airspace Congestion and Range Access

Stoke Space’s launch site is in a busy launch corridor at Cape Canaveral, alongside other space companies. Due to the high concentration of rocket launches, the Federal Aviation Administration is looking into safety changes. Given Stoke Space’s ambitions of consistent, rapid-reuse launches, a restriction on launch cadence could hurt the company’s ability to test its rocket.

Summary

Stoke Space is developing Nova, the first fully and rapidly reusable medium-lift rocket, designed to recover both stages after every flight. By targeting a 24-hour turnaround time between flights, Stoke Space aims to increase flight cadence and amortize fixed infrastructure costs across a high volume of annual missions. With a growing commercial space economy and government interest, Stoke Space is positioning itself to compete with larger launch service providers in the medium-lift segment. While Stoke Space has conducted extensive testing of its Nova rocket components, its performance and rapid reusability under real-world flight conditions remain unproven. This risk is critical as the commercial launch industry has a punishing track record. Of the 142 small launch startups active in 2006, only SpaceX and Rocket Lab have achieved repeatable, consistent orbital launch as of June 2026.